Decision and price auto loans. Deliver your yield and volume strategy.

Karus is the only programmable credit intelligence platform built for decisioning and pricing auto loans. Credit investors get access to auto loans at the yield and volume their strategies require.

66% lower

Unit default rate vs manual underwriting in head-to-head

16 of 20

Monthly vintages higher projected net unlevered yield than manual

+20 bps

Seasoned-cohort average NUY at the same APR

The challenges

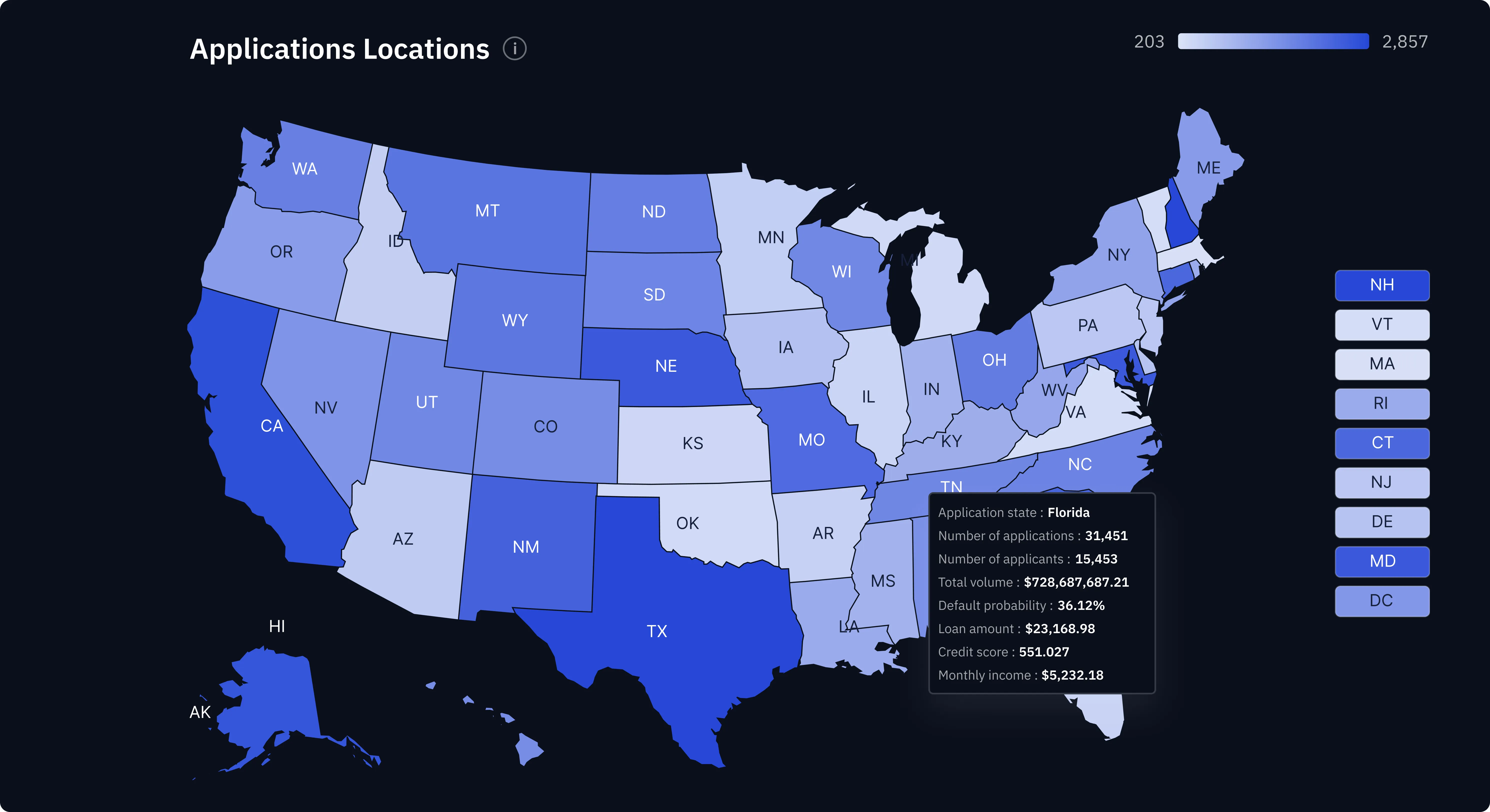

Access to quality auto loan flow is structurally constrained

The best auto loans never reach the open market. Dealers route them to preferred lenders first, through related finance companies, credit union programs, and routing platforms that embed lender preference by default. Direct buyers compete for what is left. Structured buyers and fund allocators inherit the selection-quality problem one step removed, through whichever originator they back.

Yield projection depends on data most allocators cannot access

The loan-level information available before capital commits predicts loss averages, not loss curves. Without roll-rate and seasoning data, net unlevered yield estimates rest on cumulative net loss assumptions that the available reporting cannot actually support. The estimate ends up closer to a guess than a projection, whether you are evaluating a forward-flow program, a whole loan pool, an ABS tranche, or a fund allocation.

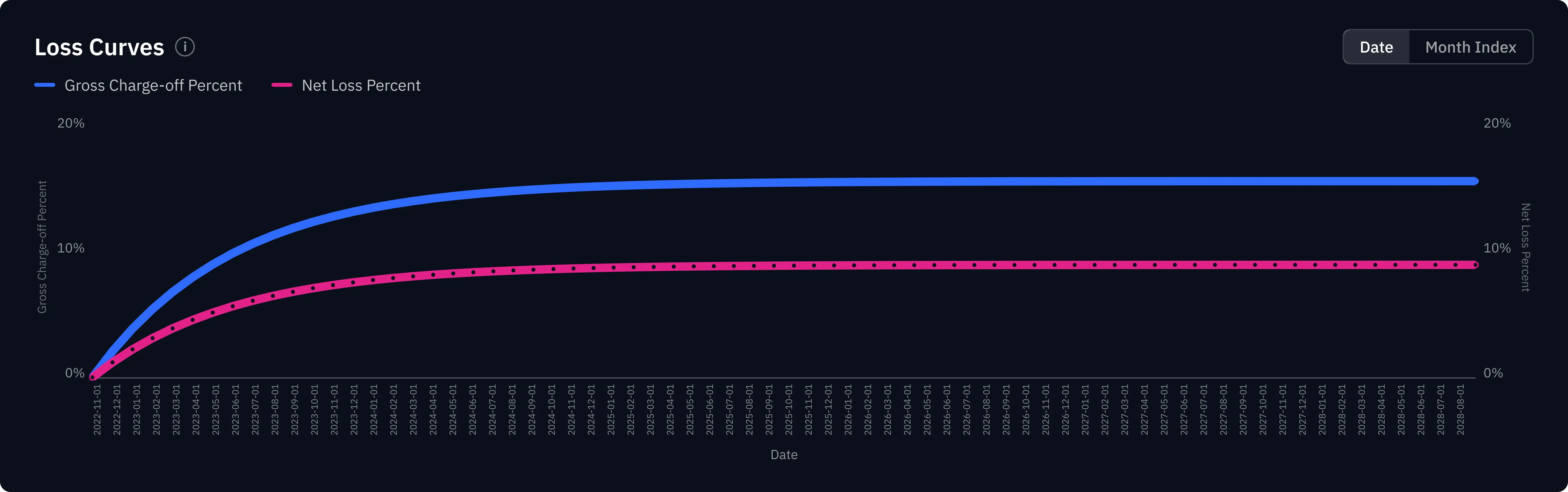

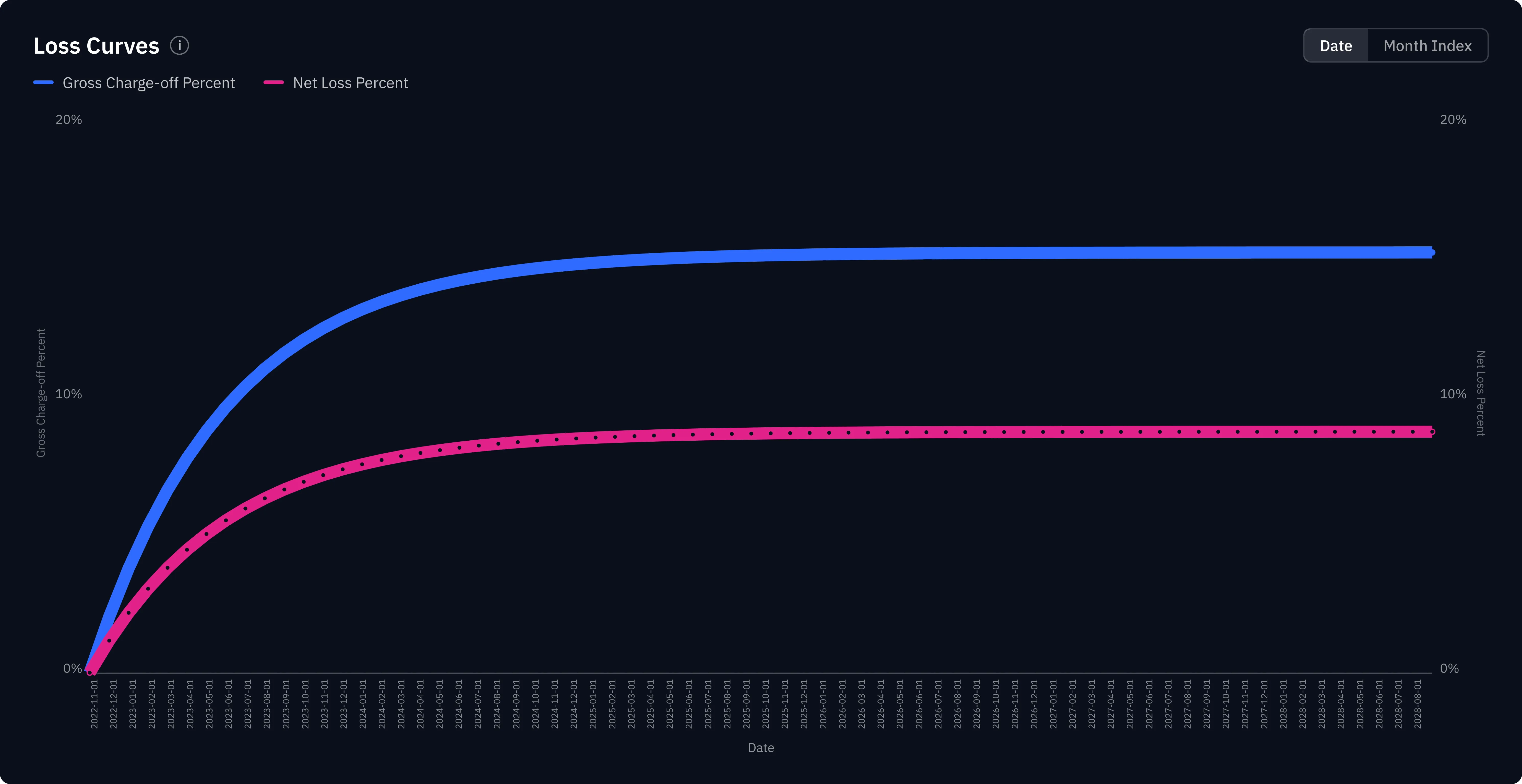

Capital partner terms depend on loss curve consistency, not loss averages

Warehouse lines, securitization tranches, and forward-flow leverage all require loss timing precision because even one bad year unravels the financing structure built around the portfolio. Wide dispersion across vintages forces larger reserve buffers and prices your paper as a range rather than a programmed outcome. Strong average returns do not earn the terms; a tight, dollar-weighted loss curve does.

Why auto finance is different

Most auto loans move through a dealer, not direct to the borrower. The originator that wins dealer acceptance has to price every loan in seconds against the borrowers credit trajectory and the specific vehicles depreciation risk, not just a current credit score. Generic credit tools score the borrower. Auto requires scoring the loan and the dealer.

The best auto loans never reach the open market. Dealers route them to preferred lenders first, through related finance companies, credit union programs, and routing platforms that embed lender preference by default. Karus-underwritten portfolios start from inside that routing stack, not from what is left at the bottom of it.

Capital partners commit on consistency, not on average returns. Forward-flow commitments, warehouse lines, and securitization tranches all require loss timing precision because even one bad year unravels the financing structure built around the portfolio. The originators underwriting quality, expressed in the loss curve and the roll-to-default behavior of every vintage, determines whether that consistency exists well before the losses become visible.

Auto finance is not just a harder version of consumer lending. It is a different problem.

Sustained yield predictability through systematic pricing

Across 20 monthly vintages of static-pool analysis on the same loan population, Karus held a dollar- weighted net unlevered yield advantage at near-identical APR. The advantage came entirely from selection quality, not from pricing: both books originated at roughly 10.5% gross APR, which isolates the comparison to who picked the better loans.

+20 bps

Seasoned-cohort average NUY with comparable cohort-level stdev (0.35% vs. 0.34%)

16 of 20

Vintages where Karus delivered higher projected net unlevered yield

55% lower

Projected lifetime cumulative net loss (0.52% vs 1.17%, pooled)

Karus tunes every layer of the cash flow waterfall

Most credit intelligence tools improve one line of the cash flow waterfall. Karus improves all of them, starting with access to the loans worth approving and tuning every line to your specific yield target.

Loan Access

Structural preference inside dealer routing channels gives Karus-underwritten portfolios first-look access to quality loan flow. A moat as defensible for investors as it is for lenders.

Gross WAC

Trajectory pricing sets each loans rate against its actual risk at acquisition, not against a static FICO band. The WAC at the top of the cash flow waterfall is a number you can underwrite to.

Less Origination

Automation compresses per-loan origination cost as volume scales. Portfolio economics stay consistent at $100M, $1B, and beyond.

Less Servicing

Better selection at origination means less servicing intervention downstream.

Less Losses

Karus models the full loss curve, the roll-to-default behavior and the recovery rate, not just cumulative net loss. Two pools with identical total losses structure very differently depending on when the losses hit. Timing is the variable most reporting leaves out.

Less Dealer Premium

Most lenders set dealer premiums by credit tier, overpaying across the board to win acceptance. Karus prices the dealer check individually for each loan. The yield retained at this line flows directly to capital.

Net Unlevered Yield

A tight, predictable yield band rather than a wide range. Lower dispersion across vintages means smaller reserve buffers and paper priced as a programmed outcome. Certainty earns better terms.

The model is only as good as the data under it

Karus loss-curve projections rest on the most complete auto loan dataset in the industry: nationwide, multi-decade payment history across millions of loans. For a capital partner underwriting a forward commitment, the depth of that training data is what separates a credible projection from a curve fit to too few outcomes.

$5B+

Origination volume processed through Karus decisioning models

$10B+

Seasoned portfolio volume scored by Karus cash flow models

100M+

Auto loan outcomes used to train Karus models

What Karus delivers

Streamlined Loan Access

Programmatic access to quality loan flow across multiple originators. Toggle originators on or off based on real performance. Lean into volume from the underwriters that are hitting your yield target, not the ones that arent.

Loss Timing Precision

Forecast net unlevered yield with precise loss curves before committing capital. Model when losses hit, not just how big they get.

Yield Consistency

Set your yield target. Karus automates delivery with the precision and predictability to hit it quarter after quarter.

One Underwriting Standard

Every Karus-underwritten loan meets the same standard, no matter the originator. Evaluate the underwriting once, apply it across every Karus-sourced loan.

AI underwriting. Programmable credit strategy for auto finance.

Karus is not competing in the AI underwriting category. It is defining a new one: programmable credit strategy for auto finance. The result is portfolio economics built on loan access, accurate loan-level pricing, and consistent outcomes that competitors cannot easily replicate.

Generic AI underwriting

Borrower score

Programmable credit strategy

Programmable engine

Evaluate a portfolio

Send us a portfolio file. We will rebuild it loan by loan through Karus and show you the projected net unlevered yield, the loss curves by vintage, and where the selection differs from manual. No commitment to commit capital. Just a side-by-side of your current process and ours.