Auto finance isn't a harder version of consumer lending. It's a different problem.

So we built Karus for that problem. Predictive technology that decisions and prices every auto loan, so originators and investors hit the portfolio outcomes their strategies require.

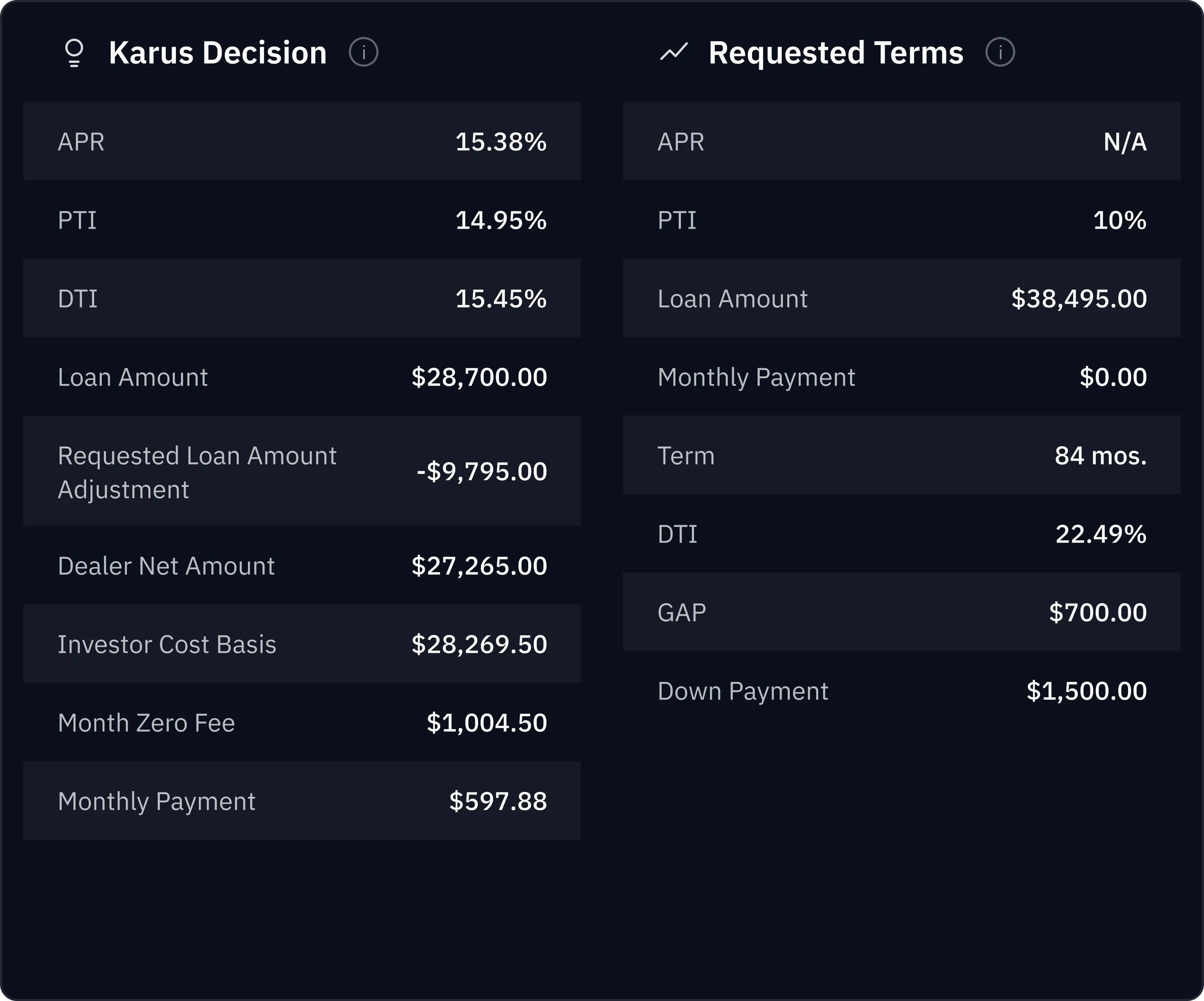

.svg)

Auto lending runs on tools built for a different job

Auto finance is one of the largest consumer credit markets in the country, second only to mortgages, with roughly $700 billion in new loans originated every year. And it doesn't work like the rest of consumer lending. Most auto loans move through a dealer rather than direct to the borrower. The dealer shops each application to several lenders at once, and the lender that wins dealer acceptance has to price the loan in seconds against the borrower's credit trajectory and the specific vehicle's risk.

On the other side of that market, credit investors buy those loans. Forward-flow buyers, whole-loan purchasers, and ABS issuers commit capital against portfolios whose yield depends entirely on how well each loan was underwritten at origination.

Both sides run on tools built for other problems. Generic models score the borrower. Rules engines designed for personal loans and mortgages were adapted to auto, and they miss the dealer dynamic, the collateral risk, and the loss timing that actually decide the outcome. A market this large is underwritten with instruments built for a different job.

What I learned the hard way

After Random Forest Capital was acquired in 2018, I went looking for the next problem to solve with data and predictive technology. Auto seemed obvious: big market, lots of data, mispriced risk everywhere. We had a great model, but we couldn't get the portfolio to perform. It took me longer than I'd like to admit to work out why. Auto isn't a harder problem than other lending, it's a different one. Here's what I learned the hard way.

01

There's a dealer in the middle

Dealers shop every application to several lenders at once. Lose on price, structure, or response time and you get nothing. Everything starts with winning dealer acceptance.

02

A FICO score is a point, not a direction

A 650 trending toward 700 isn't the same loan as a 650 trending toward 600. Most tools price them the same. Real money sits in that gap.

03

You score the loan, not just the borrower

A car carries its own risk. Generic tools score the borrower, but in auto you score the loan. A 90,000-mile car that breaks down at 120,000 isn't a good five-year note, no matter who's signing.

04

The best loans never hit the open market

Dealers route them to their preferred lenders first. Without a structural position in that flow, you're underwriting what's left. A better model doesn't fix that.

05

Systematic beats discretionary at scale

Experienced underwriters have real instincts, and they're valuable. But applied loan by loan, those instincts can't hold a portfolio to a consistent loss curve across thousands of decisions. The instincts don't go away. They get encoded and amplified.

The people behind the model

Leadership team

Karus is built by a team that has worked this problem from both sides, credit and data science. The convictions above are not theoretical. They come from people who have priced auto risk and built the models that do it.

A founder with a deep capital-markets background. More than a decade running institutional Nasdaq trading desks, then co- founded Random Forest Capital, the credit and data-science firm acquired by Franklin Templeton in 2018. He started Karus to bring that mix of markets, credit, and data to auto finance.

A data scientist who builds machine learning into production. Applied data science at the World Bank and Grant Thornton, then founded Sphaeric.ai, building end-to-end ML systems for clients. He leads the data science and technology behind the platform.

Board of Directors

Karus is governed by a board that pairs deep credit and capital-markets pedigree with early-stage company-building. Between them they have priced risk, allocated institutional capital, built credit businesses at scale, and backed founders from the first check. They understand auto finance as the capital-markets problem it is.

Keri Findley

Founder and CEO, Tacora Capital

A private-credit and asset-based lending investor. She founded Tacora Capital, a private-credit firm that provides debt capital to venture-backed companies, and earlier spent eight years at Third Point building and running structured and distressed credit investing. She brings the perspective of the institutional credit that funds and buys loan portfolios, the seat closest to the outcomes Karus is built to deliver.

Jason New

Vice Chairman of Investment Banking, Lazard

A credit and special-situations investor with more than two decades in institutional credit. He spent fifteen years at GSO Capital Partners, now Blackstone Credit, as an original partner and Global Co-Head of Distressed and Special Situations Investing, later led Onex Credit Partners, a $25 billion alternative credit manager, as chief executive, and is now Vice Chairman of Investment Banking at Lazard. He brings a capital-markets and structured-credit lens to how Karus portfolios are built and financed.

Mike Self

General Partner, StageDotO

An early-stage venture investor and one of Karus's earliest backers. He is a General Partner at StageDotO, an early-stage fund that backs founders building ambitious companies, and has served on the Karus board since 2021. He brings the conviction of an investor who has been with the company from the start.

What our platform enables

Those beliefs are built into one platform. Karus is programmable credit intelligence: predictive technology that decisions and prices every auto loan to the strategy you set, then holds the whole portfolio to that target.

For loan originators, that means winning dealer acceptance with loan-level pricing in seconds, then building a portfolio that performs. For credit investors, it means access to quality loan flow and the loss timing precision to predict yield before capital commits. Both sides program their own strategy for yield target, risk appetite, and dealer mix, rather than accepting a fixed model.

This is what we mean by programmable credit strategy. Not a better score, but a platform you configure, then hold to the number you promised.

Where Karus stands today

Lenders underwrite roughly $50 million in auto originations on the Karus platform every month, and it has been tested where it counts. In a 20-month head-to-head against a 15- person manual underwriting team, on the same loan population, Karus cut the unit default rate by two-thirds and delivered higher projected net unlevered yield in 16 of 20 monthly cohorts. Karus sources that loan flow through partnerships most platforms cannot replicate: through Automatic USA, CRIF, and DOFC, the platform holds structural preference inside dealer routing channels.

$50M+

Auto originations underwritten through Karus each month

66% lower

Unit default rate versus a manual underwriting team, head-to-head

16 of 20

Monthly cohorts where Karus delivered higher projected NUY

AI underwriting. Programmable credit strategy for auto finance.

Karus is not competing in the AI underwriting category. It is defining a new one: programmable credit strategy for auto finance. The result is portfolio economics built on loan access, accurate loan-level pricing, and consistent outcomes that competitors cannot easily replicate.

Generic AI underwriting

Borrower score

Programmable credit strategy

Programmable engine

See it on your own portfolio

Wherever you sit in auto finance, the conversation starts with a portfolio.

Bring us a sample of your origination volume. We will run it through Karus and show you, loan by loan, where the platform would have approved differently, priced differently, or held back.

Send us a portfolio file. We will rebuild it loan by loan through Karus and show you the projected net unlevered yield, the loss timing curves, and where the selection differs from manual.